Learn how to Boost your financial future with SMSF & Property

Posted 26 Feb '24

Posted 26 Feb '24

Disclaimer: This content is for informational purposes only and does not consider your personal

financial circumstances. Please conduct your own research and consult with a qualified financial advisor before making any investment

decisions. Investments carries inherent risks, and individual circumstances may vary.

The typical Aussie battler loves Australian real estate. The old faithful of bricks and mortar has been the bedrock of our economy for the past 30 years. A report by Core Logic shows that we have had 6 cycles of growth for a national average growth of 382% within that period. It is physical and we know we can rent it out to generate an income.

Australia's real estate market has long been considered a safe and lucrative investment avenue. With a stable economy and a consistently growing property market, it's no wonder that many Australians view property as a key component of their investment portfolio.

One pain point we often hear from clients is the fact that their superannuation fund doesn’t directly invest into property. In this article, we are going to explore the only legal way to borrow and acquire property in super which is via a self-managed superannuation fund (SMSF).

In its purest form, a SMSF is no different from any other superannuation fund; it is a special purpose trust where the assets are managed

for its beneficiaries for the sole purpose of providing retirements benefits.

However, with a SMSF you have full autonomy to control the decisions of your fund’s investments. This of course extends to all types

of real estate including residential, commercial, industrial, and business real property to name a few.

Tax benefits on income and gains

Acquiring property through an SMSF opens the door to generating rental income. This can be a steady source of revenue that contributes to

the fund's overall growth.

Rental income, when reinvested, can compound over time, adding a valuable income stream to support retirement goals along with the capital price appreciation.

One of the primary advantages of using an SMSF to invest in property is the potential for tax benefits. SMSFs enjoy concessional tax rates at 15% flat rate on both its net rental income and capital gains. If the property is held for over 12 months, the capital gains is reduced by a further 33.33%.

In retirement phase, the fund switches from being taxed at 15% to 0% up to a limit per member of $1.9 million from 1 July 2023 (called the transfer balance cap). The idea to realise capital gains when the SMSF is in retirement phase as to reduce CGT further.

Flexibility

While traditional superannuation funds often limit investment options to a prebuilt portfolio (conservative, balanced, growth), SMSFs allow

trustees to expand their portfolio. Including property in your SMSF can be a strategic move to balance risk and potentially enhance

returns.

Control

SMSF trustees have a high level of control over their investment decisions. This control extends to property selection, management, and

divestment.

For those with a keen interest or expertise in real estate, this control can be a valuable aspect. Additionally, the flexibility of SMSFs

allows for strategic decision-making, adapting to market conditions and individual financial goals.

Scale

Scale and access can also be increased as SMSFs can have up to 6 members. Having scale in turn leads to economies of scale which can reduce

overall fees as this can be shared across more members. High capital can also lead to better investment opportunities within the real

estate market.

Estate planning

This control and flexibility also extends to estate planning if a member were to pass away. The SMSF deed may provide who and how these

benefits are to be distributed as along as it aligns with super regulations.

The successor trustee can cascade nominations, exclude beneficiaries, and tie this together with your will for asset protection and

planning. Distributions can also be made to tax dependents to allow the most optimal tax position.

While advantages of incorporating property into an SMSF are apparent, it is equally important to be mindful of certain considerations and

potential challenges with SMSFs.

For instance, property transactions within an SMSF must adhere to strict regulations to ensure compliance with the super and tax law. This

includes:

The trustees also have important responsibilities including:

To make informed and prudent decisions in the best interests of the SMSF members

Trustees should also be aware of liquidity concerns, as real estate is inherently less liquid than other asset classes. Moreover, managing property within an SMSF requires a thorough understanding of property markets, property management, and compliance requirements. Time & personal interest is also a factor in managing a SMSF.

It is imperative that you engage professional advice, such as that from financial advisors, accountants, legal experts, and property agents to allow you to navigate these complexities successfully. This will obviously come at an additional cost to the SMSF.

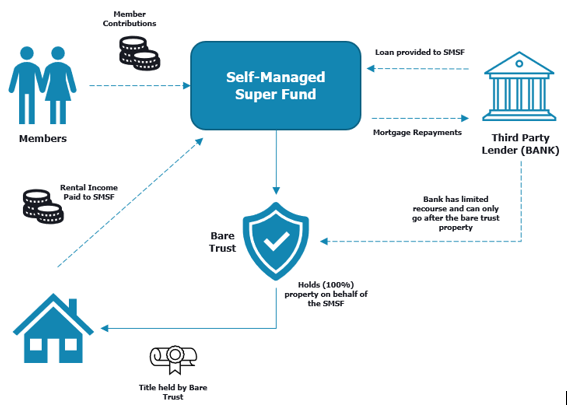

As mentioned previously, SMSFs is probably the only structure where the ATO allows for superfunds to borrow funds to acquire property (single acquirable asset). The method in which this is achieved is called a limited recourse borrowing arrangement (LRBA for short).

Below is a diagram which demonstrates how a LRBA works:

At a high level, a LRBA involves the SMSF taking out a loan from a lender to then acquire a property to be held in a separate (bare) trust. Any rental returns are paid to the SMSF and that along with other means for cashflow (such as member contributions) are used to make mortgage repayments back to the lender.

If there is ever a default, the lenders rights are limited to the asset held in the separate (bare) trust. In other words, they have no recourse against other assets of the SMSF. This is designed specifically to protect SMSF members.

Whilst it is possible to borrow under an LRBA, other important aspects to consider include:

SMSFs have emerged as a powerful vehicle for Australians looking to take control of their retirement savings and explore diverse investment opportunities. Acquiring property within a SMSF presents a strategic avenue to capitalise on the stability and growth potential of Australia's real estate market.

As with any investment strategy, thorough research, adherence to regulations, and professional guidance are imperative for success. If you are interested in exploring the topic further, please give us a call on 07 3124 0244 and we are more than happy to provide further information or put you in touch with a qualified financial advisor to begin your journey on the SMSF property ladder.

Many business owners think tax planning means meeting with their accountant in June and finding a few last-minute deductions before the end

of the financial year.The reality is that true tax planning starts much earlier in the year.

For established businesses, proactive tax planning isn’t about scrambling to reduce tax at the last minute. It’s about creating a strategy

throughout the year that supports business growth, improves cash flow, and helps owners make better financial decisions.

For many small business owners, the end of the financial year (EOFY) feels like the finish line. Once tax planning is complete, financial statements are prepared, and compliance obligations are lodged, it is tempting to return to business as usual.

Looking for the best accountant in Brisbane? Learn what to look for in an accountant, from proactive advice and communication to tailored support for growing businesses.