Keep your wealth health strong with a holdings company

Posted 6 Feb '22

Posted 6 Feb '22

As you progress through this journey called ‘entrepreneurship’, you will find that each stage of the business comes with different challenges and concerns.

At the start-up phase, you were simply trying to get your minimum viable product to market. During the growth phase, you competed for market acceptance and gaining market share. With maturity, the focus was then turned to ensuring the enterprise is sustainably profitable whilst reaching out to new segments.

Once the business starts to generate surplus cash reserves over and about what is necessary for working capital (and the business is financially comfortable), the next thing on your mind then generally turns to:

and you start to ponder – “how do I see personal benefit from this wealth now and into the future by using it to invest, purchase real estate property or acquire further ventures or equities?”

Realistically the 0.02% interest on saving is a net negative real return when you take into account inflation of 2-3% per annum. We all know billionaires make money from capital and not trading labour for money.

Don’t get me wrong, wealth health is the end game. But it is also imperative that we do this in a manner in which your hard earn cash is not compromised in the event of unforeseen circumstances and without (you guessed it) paying too much tax!

This is where a Holdings Company can come into play.

So before we take you on this magical journey of the Holdings Company, there are a couple of conditions that need to me meet with regards to your business structure. This is where you are structured with a private operating company that carries on the business; where the shares are wholly owned by a discretionary (family) trust. This is depicted in the diagram 1 below.

Diagram 1 – Trading Company Structure with family trust as shareholder

If you want to learn more about the importance of getting your structure right, please read my article on this here: getting-some-structure-in-your-life.

Acquire in the Business Entity (private limited company)

The most simplistic way to acquire the investments is in the operating company, and whilst it does not result in funding issues, it does however expose the wealth and cash to business and regulatory trading risk.

In the event of a successful lawsuit or unforeseen circumstances on the business, all your wealth is now exposed. Whilst it is important to accumulate wealth, it is equally vital to protect it. So, this option is not viable. Good for tax, bad for asset protection. Moving on!

Acquire in the Shareholding Entity (discretionary [family] trust)

The most obvious the method to limit the exposure and risk is to employ the basic segregation strategy (e.g. acquire the investments in the passive family trust). However to do this, the operating company will need to extract that wealth (equity) from the company.

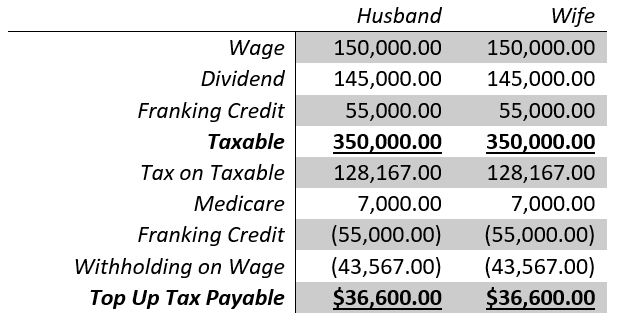

For example, let’s assume on a conservative basis that there is $290,000 worth of retained earnings in the operating company. This would be extracted by paying a fully franked dividend equal to the wealth in the company ($290,000).

This will achieve full asset protection benefits because there is now no equity in the operating company which is exposed to trading risk and in the event of insolvency of the company, there is nothing for creditors to take.

Although the shareholder is a trust in this case, where it will have discretion to distribute this dividend, ultimately a trust is a flow through entity. It must make a distribution of trust income to beneficiaries by 30 June each year or be subject to 47% penalty tax.

If there are no other beneficiaries besides the typical patriarch of the family and their spouse, the distribution will need to go to them and thus also result in quite significant levels of top up tax. See below:

As such, there is an additional $73,200 top up tax; leaving only $218,800 remaining to be used for investment. So, the strategy is good for asset protection, but bad for tax effectiveness.

Can the company lend the money to the Family Trust for investment?

Unfortunately no!

Without getting all tax nerd on you, if a private company makes a loan to a trust, it will be caught under the deemed dividend rules; meaning the ATO will treat the loan as an unfranked dividend in any case. From a tax perspective, this is worse that because we are unable to claim the franking credits on the dividend. The top up tax in the above scenario on $290,000 is a whopping $183,200.

Although you can manage the repayment of this loan over 7 years (under what is known as a complying loan agreement), the issue is that until the loan will still represent an asset on the balance sheet for the $290,000. This does not solve the asset protection issue as the ‘loan asset’ can still at risk from creditors in insolvency.

In a worst-case scenario, the trust would need to sell its investments to then pay back the company to then settle potential creditors or lawsuits nevertheless (it forces a liquidation event on the trust).

Whilst it is not as bad as purchasing the investments directly in the operating entity in the first instance, it potentially still leaves the wealth exposed.

But is there a way to deal with both the asset protection & tax issues?

Enter the holy grail of corporate structuring > the Holdings Company strategy!

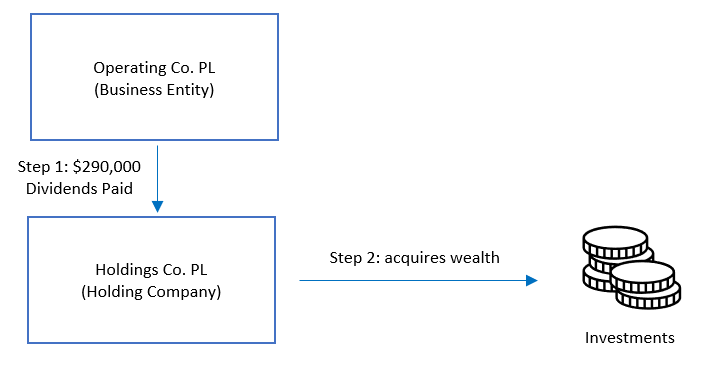

The final alternative to achieve both asset protection and no top up tax is to perform what is known as a holding company restructure. This is where we layer the structures so that there is a head entity and subsidiary companies (as implemented with listed public companies).

Diagram 2 – Change from Current to Holdings Structure

Diagram 3 – Equity Cash Out + Investment

The difference here is that the Holdings Company can retained the dividend received as opposed to the family trust which is effectively a

flow through entity. When the dividend is paid, the cash out of equity ensures that there is no wealth exposed to operating risk at the

business level; as the Holdings Company essentially acts as a safe haven.

Another key benefit from a tax perspective is the fact that the dividend from paid to a wholly owned company (called a non-portfolio dividend) is considered to be active income and thus not subject to top up tax. Accordingly, there is no additional tax on the dividend under this scenario.

It is important to note that whilst the Holdings Company is not eligible for the CGT discount, all income and capital is taxed at a flat rate of 30%. If the idea is to build up wealth in the longer term where the funds can be reinvested in a concessionally tax environment, then this structure would be the most effective strategy to implement (kind of like a second super fund without the onerous rules).

Ultimately, the Holdings Company can still pay a dividend to the trust to them stream these distributions when it is tax optimal to do so. A great example of this to pay dividends in retirement so you can receive refunds of the excess franking credits.

Whilst we all scramble day to day in building a profitable business to enable us to live the lifestyle we want; it is equally important to treat and protect your wealth health seriously. You can spend an eternity building this to have something unpredictable wipe the slate clean.

So whether you are a seasoned business owner seeking a corporate reorganisation or simply would like an investment structure for your wealth building goals, give us a call today on (07) 3124 0244 to leave your legacy with confidence!

Leonard Jiang | CA, CTA, DFP

Partner

Tax Specialist

When you plan with intention - and pair it with accountability - you’re not just hoping things will work out. You’re building a business that will.

.jpg)

Let’s face it; bookkeeping isn’t the most exciting part of running a business. However, it’s one of the most important! Keeping your financial records in check not only helps you stay on top of your business but moreover ensures you're meeting Australian Taxation Office (ATO) requirements without stress or penalties.

.jpg)

For Not-for-Profit (NFP) entities, understanding and adhering to new requirements can be a daunting task, especially with the ever-evolving regulatory landscape.